Preliminary results for the year ended 31 December 2023

Oxford Nanopore Technologies plc (LSE: ONT) ("Oxford Nanopore" or the "Group"), the company behind a new generation of molecular sensing technology based on nanopores, today announces its preliminary results for the year ended 31 December 2023.

Gordon Sanghera, Chief Executive Officer, commented:

"We delivered strong underlying revenue growth of 39% in 2023, driven by the strength of our differentiated technology, commercial model, and strategic investments in infrastructure. Last year we also delivered breakthroughs in our platform performance, achieving record accuracy, expanded end-to-end workflows and increased access to high output applications with the PromethION 2 (P2) product rollout, with 700 P2 Solos sold or leased through starter packs in FY23.

"As we look forward, our highly differentiated platform and substantial market opportunity, positions us well to deliver long-term, sustainable growth. We are focused on key strategic initiatives to drive value, including disciplined investments in our technology and commercial operations where appropriate to unlock key opportunities in priority markets. We also remain mindful of end-market conditions, with sales cycles lengthening at the same time as we have expanded our commercial and operational infrastructure to support future growth. These factors have led us to revise our forecast for achieving adjusted EBITDA breakeven to the end of 2027 as we continue to focus on delivering against the huge commercial opportunity ahead of us.

"We are confident that we can deliver underlying revenue growth of 20 to 30% in 2024 and greater than 30% in the medium term."

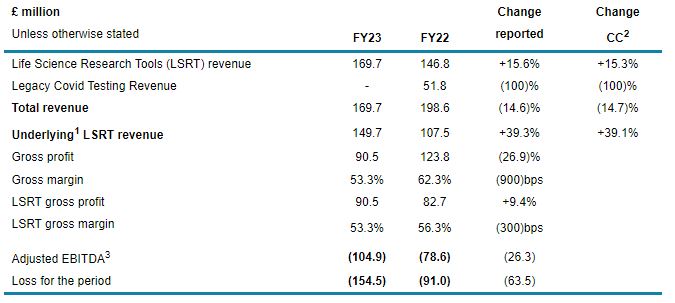

Summary financial performance

Notes:

Certain numerical figures included herein have been rounded. Discrepancies in between totals and the sums may occur due to such rounding.

1 Underlying revenue excludes revenue from COVID sequencing and revenue from the Group's largest customer, The Emirati Genome Program (EGP). All references to underlying growth in this document have been adjusted for COVID sequencing and EGP revenues.

2 Constant currency applies the same rate to the FY23 and FY22 non-GBP results based on FY22 rates.

3 Adjusted EBITDA is the EBITDA adjusted for i) Share-based payment expense on founder LTIP ii) Employer's social security taxes on Founder LTIP and pre-IPO awards, iii) Revenue and expenses associated with the settlement of the COVID testing contract with the DHSC iv) Gain on the sale of property and v) impairment of investment in associate - see note 5(b).

FY23 Financial highlights

- Life Science Research Tools (LSRT) revenue increased by 15.6% to £169.7million; underlying revenue excluding revenue from the Emirati Genome Program (EGP) and COVID sequencing of £12.0 million and £8.0 million respectively, was £149.7 million, an increase of 39% in the period.

- LSRT revenue growth led by the Americas with revenue up 27% (48% on an underlying basis) and EMEAI with revenue up 16% (50% on an underlying basis).

- Strong underlying growth was achieved across all LSRT customer groups, with the highest-spending S3 customers increasing the most, growing 69% in the period.

- Underlying revenue, excluding EGP and COVID, grew fastest across the PromethION franchise, representing all devices and flow cell sales from the PromethION product range, up 83% in the period to £48.8 million (FY22 £26.6 million). Underlying revenue from the MinION franchise, representing all sales of MinION flow cells and devices that run MinION flow cells (including GridION and MinION) grew 14% to £58.8 million (FY22: £51.5 million). Other revenues, representing kits, services revenues and other devices grew 44% on an underlying basis to £42.2 million (FY22: from £29.4 million).

Total revenue and gross margin decline of 14.6% and (900) basis points respectively, reflects:

- The previously announced conclusion of the Group's legacy Covid testing contract with the Department of Health and Social Care (DHSC) in 2022, plus

- 300 bps decrease in LSRT gross margin to 53.3%, predominantly reflecting the one off and short term impacts from i) the G42 contract (the Group's agreement to the supply of sequencing tools in support of, the EGP was amended in December 2023) ii) the write off of excess COVID sequencing kits and legacy devices alongside; and iii) upgrading the compute on large PromethION devices, an investment that enables real time basecalling. These headwinds were partially offset by underlying improvements in flow cell margins, particularly across the MinION range, in relation to both yields and recycling rates.

- Excluding these one-off items the underlying LSRT gross margin was 58.8% (FY22: 58.0%).

- ·Adjusted EBITDA loss of £(104.9) million (FY22: £(78.6 million)); higher LSRT gross profit offset by increased operating expenses, reflecting investment in commercial and marketing teams, in innovation to support new product development and manufacturing and logistics infrastructure, to support long term sustainable growth.

- Increase in loss year-on-year to £(154.5) million (FY22: £(91.0) million). Taking into consideration that the result for FY22 included i) the income from the conclusion of the Group's Covid testing contract with the DHSC as described above, a net benefit of £37.9 million and ii) the impact of the gain on disposal of property of £18.6 million; the balance of the increase in loss was primarily due to increases in operating expenditure in the year, offset partially by a reduction in the share based payment and associated costs, an increase in finance income as well as the increase in Gross profit from LSRT.

- Strong balance sheet; cash, cash equivalents and other liquid investments of £472.1 million[1] as at 31 December 2023, compared to £558.0 million as of 31 December 2022. In October 2023, bioMérieux SA (bioMérieux) agreed to subscribe for 29,025,326 shares at a subscription price of 238.08p per share which equated to a total investment of nearly £70 million.

See the financial review for further detail.

FY23 Business highlights

- Delivered a net increase of more than 750 active customer accounts in the period, taking total active accounts to more than 7,600 in 2023; new customers will be key driver of consumables sales in future years.

- Execution of 2023 innovation goals including higher accuracy chemistry, PromethION 2 (P2) Solo launch, direct RNA upgrades, basecalling acceleration and expansion of our informatics products, further differentiating our platform and broadening demand for our technology.

- Approximately 2,800 peer-reviewed research papers published by users of Oxford Nanopore technology in 2023, bringing the total to approximately 11,000 to date, showcasing breakthrough research across cancer, human genetics and infectious disease and demonstrating continued opportunity for growth in the genomics research market.

- New strategic collaborations added to develop and access new growth markets in clinical and industrial applications, including collaborations with the Mayo Clinic to advance research in cancer and bioMérieux to develop products that serve the infectious disease diagnostics market.

- Strategic investment from bioMérieux, strengthens existing collaboration, which is accelerating expansion of Oxford Nanopore's technology into infectious disease diagnostics.

- Expansion of commercial teams, including strategic leadership hires to increase traction in key markets across the Americas, EMEAI and APAC. Commercial infrastructure is capable of supporting the Group's development over the coming years to drive long-term sustainable growth.

- Expansion of the leadership team, post period end, to support the business in its next phase of growth: Nick Keher appointed as CFO and Director of Oxford Nanopore, adding significant financial leadership experience and a deep understanding of global capital markets. Nick succeeds Tim Cowper, who moves into a new role as Chief Operating Officer and will lead Oxford Nanopore's continuous improvement programmes and expanding international footprint and operations.

- Expansion of the Board with three new Non-Executive Directors, including Kate Priestman who adds extensive experience as a biopharma executive, Dr Sarah Fortune, an academic focused on infectious disease including TB, and Dr Heather Preston, a long-time biotech and life sciences investor, with significant experience as a director of technology-based healthcare companies

- Post year end, the Group announced the retirement of Dr James ("Spike") Willcocks, Clive Brown, and Tim Cowper from the Board as part of normal Board evolution and in line with best practice governance. As part of the Group's commitment to board diversity, this evolution will support progress towards fulfilling the goal of reaching 40% female Board representation. Following the AGM in June 2024, the Board will include two executive Directors and seven Non-Executive Directors, three of whom are women.

See the business review for further detail.

- FY24 Financial guidance

We expect full year 2024 LSRT revenue of between 6-15% growth on a constant currency basis, equating to £180 million to £195 million at current exchange rates which is 20-30% growth on an underlying basis, when excluding known headwinds from COVID sequencing of approximately £8 million as well as a year‐over-year headwind of up to £12 million from the revised amendment to the Group's agreement with G42 in supply of sequencing tools in support of the EGP. EGP and COVID sequencing are not expected to contribute meaningfully to group revenue in 2024 and as such any revenue will be reported as underlying growth from 2024 onwards.

Whilst revenues are expected to increase across each customer segment, we expect to see faster growth among S2 and S3 customers, driven by continued roll out of the PromethION franchise, alongside growth across indirect channels. Geographically, it is expected that growth will be highest across the Americas and EMEAI regions in 2024.

There continues to be a material opportunity for Oxford Nanopore to penetrate, reshape and expand the market, leading to above end market growth. However, this is balanced against the backdrop of a subdued funding environment for some of our end markets due to macroeconomic factors, specific dynamics within the LSRT market alongside geopolitical concerns that have amplified since 2022.

We expect LSRT gross margin to be approximately 57% in FY24 reflecting continued operational improvements including, automation, improved manufacturing process and recycling of electrical components expected to be offset by i) growth in the installed base across the PromethION franchise as customers utilise the inclusive consumables in advance of converting to higher margin regular flow cell orders, and ii) changes to pricing across our MinION franchise to drive further adoption, with planned improvements on margin to offset this impact in future years.

There are a number of higher value, pioneering project opportunities the Group is prospecting that could accelerate growth to the top end or above FY24 revenue guidance. However, these would also likely be dilutive to gross margin in the short term as initial phases of projects complete before becoming longer term, higher margin consumable reorders thereafter as Oxford Nanopore technologies become embedded within customer workflows. The impact of these potential wins have been considered in the short and medium term margin guidance.

During 2024 we will see the annualised cost from investment in our headcount and infrastructure to support our ambitions. In order to support improving profitability going forwards, we are assessing current and future investments with a focus on greater prioritisation of activities to deliver on our growth objectives whilst supporting a strong ROI.

Revised medium term guidance

Given the end-market dynamics previously discussed and reflected in our 2024 guidance, we have revised our medium- term adjusted EBITDA breakeven target to FY27 from FY26. This guidance reflects:

- Revenue growth of more than 30% on a compound annual growth rate at constant currency between FY24 and FY27, in-line with historical performance

- Gross margins to continue to improve and exceed 62% by FY27 as we incorporate the potential mix impact from driving top line growth

- An increased focus on financial discipline to leverage the infrastructure the company has already built and to modulate investment relative to the outlook.

The Group remains strongly capitalised with adequate resources to implement our business plan to and through EBITDA breakeven in 2027 and deliver on the significant growth opportunity in front of us.

Presentation of results

Management will host a conference call and webcast today, 6 March, at 8:00am GMT. For details, and to register, please visit https://nanoporetech.com/about-us/investors/reports. The webcast will be recorded and a replay will be available via the same link shortly after the presentation.

For further details please contact ir@nanoporetech.com